Marketplace Outlook: Closing week, there used to be force at the Indian inventory marketplace. The benchmark index broke 1.8% to with regards to the low of August after america executive imposed further price lists on Indian items. Amidst the super promoting of FII, even the massive purchases of DII may just now not take care of the marketplace. Alternatively, there used to be a slight reduction from a possible aid in GST price, higher monsoon and expectation of fed price deduction in September.

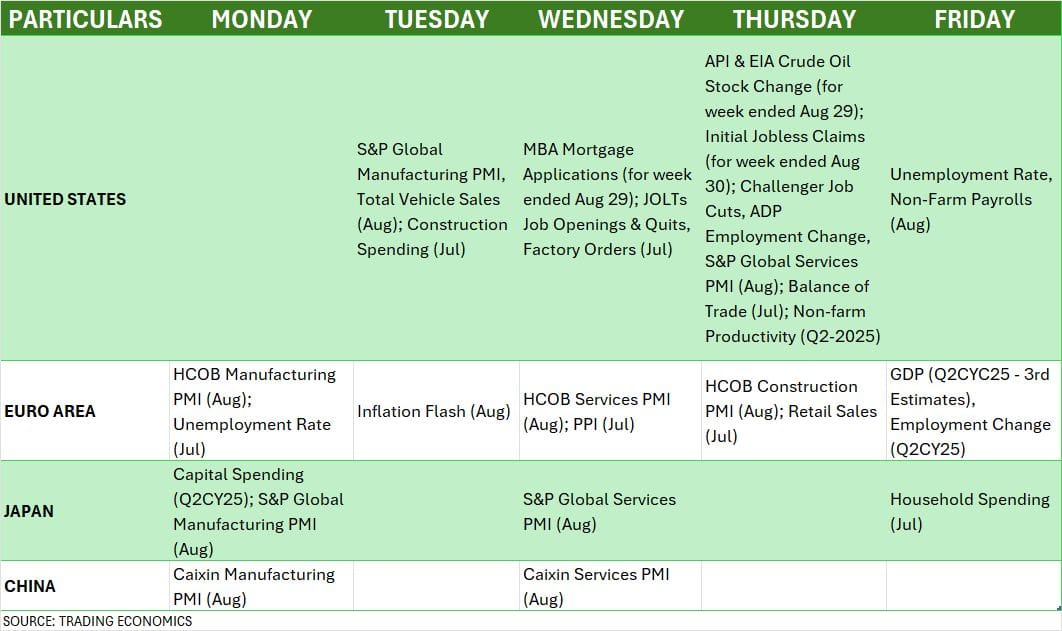

The marketplace will react to the improvement associated with GDP information higher than anticipated within the first quarter on Monday and the 4 -day seek advice from of Top Minister Narendra Modi (29 August -1) to Japan and China. In step with mavens, the week ranging from 1 September is prone to stay in a restricted vary. All through this time, the GST Council assembly, auto gross sales, US process information, production and products and services PMI quantity and Indo-US industry negotiation will probably be an eye fixed in the marketplace.

Siddharth Khemka, the analysis head of Motilal Oswal Monetary Products and services, mentioned, ‘We estimate that the marketplace will stay in a restricted vary. it PM Narendra Modi’s most sensible leaders of Japan and China Will focal point on strategic conferences with Ok. On the identical time, Vinod Nair, analysis head of Geojit Investments, believes that the marketplace can display a blended perspective.

Let’s find out about the ones 10 necessary issue, which can make a decision the situation and route of the marketplace subsequent week.

GST Council Meet

On the home stage, everybody’s eyes will probably be at the GST Council assembly to be hung on September 3-4, through which a last choice will probably be taken concerning the slab. This assembly is going down at a time when an extra 25 p.c tariff has been carried out on American items from 27 August. This has affected sectors like textile, shrimp, sneakers, chemical and jewelery.

Most mavens consider that the GST reform will probably be finalized and carried out in September itself, ie prior to Diwali. Sooner than this, the concessions and tax deduction declared within the funds will make stronger the marketplace’s sentiments and intake on time.

In step with executive proposals, quickly the 2-per GST machine (5 p.c and 18 p.c) is also acceptable. This may come with many sectors together with fertilizer, textile, sneakers, medications, surgical pieces, scientific gadgets, schooling, paper. This knowledge has been given by means of CNBC-TV18 quoting assets.

Globally, the entire markets will probably be eyeing the unemployment price of August and non-form payrolls information after July Jolts Jobs Openings and Quits studies. This will probably be necessary in deciding the following coverage of Federal Reserve. GDP revision and estimated PCE figures have already indicated the potential for price minimize within the September coverage assembly.

Kaynat Chainwala of Kotak Securities mentioned, ‘Not too long ago Fed Chair Powell has pointed to the chance happening within the exertions marketplace. In this type of scenario, if there’s a weak spot within the August process document, then the topic of coverage consuming will probably be additional reinforced.

The overall figures of August Production and Products and services PMI will probably be launched from primary international locations like america, Eurozone, Japan and China subsequent week globally. As well as, August’s flash inflation, July retail gross sales information and the June quarter of Eurozone may also be in the focal point.

Production and Provider PMI

Subsequent week, many necessary figures at the home entrance can even decide the route of the marketplace. The overall figures of the producing and repair PMI of August will probably be launched on 1 September and three September. In step with preliminary estimates, HSBC Production PMI in August reached PMI 59.8 and Provider PMI 65.6, higher than the overall print of July 59.1 and 60.5.

As well as, the main points of the week’s foreign currency reserves finishing on August 29 will probably be launched on 5 September. The reserves declined to $ 690.72 billion within the week ended on August 22, whilst it used to be $ 695.11 billion previous.

Center of attention on auto cells

Car gross sales figures of August may also be declared subsequent week, which will probably be carefully monitored by means of traders. This may purpose a stir in stocks of Tata Motors, Mahindra & Mahindra, Ashok Leyland, Bajaj Auto, Hero Motocorp, TVS Motor, Eicher Motors and Escher Motors and Escorts.

FII-DII Actions

The perspective of Overseas Institutional Buyers (FII) is these days a question of outrage for the marketplace. He made competitive promoting ultimate week because of trade in tariff insurance policies and prime valuation. Closing week, FII offered stocks price Rs 21,152 crore, inflicting the overall promoting of August to achieve Rs 46,903 crore. It used to be Rs 47,667 crore in July. Alternatively, he maintained buying groceries in the principle marketplace.

Alternatively, Home Institutional Buyers (DII) ceaselessly supported the marketplace and acquired at each decline. He made a purchase order of Rs 28,645 crore ultimate week and Rs 94,829 crore in August, which is the most important per month internet buying groceries since October 2024.

Rupee at report low

In the meantime, the rupee additionally stays a question of outrage for traders. On Friday, the rupee fell 0.66 p.c to near at 88.12 in line with buck, which is the bottom stage ever. It reached 88.31 in Intrade. Lengthy bullish candles had been made at the forex chart and all of it confirmed buying and selling above the transferring moderate, thereby indicators of brief time period force.

The Indo-US industry struggle, the hedging call for of the importers and the FPI outflow have higher the force at the rupee. Alternatively, it’s running for partial reduction for exporters. Anindya Banerjee, the pinnacle of Kotak Securities and Commodity Analysis Anindya Banerjee, mentioned, “Rupees are nonetheless underwelled in comparison to their rising marketplace colleagues. Alternatively, within the close to length, industry struggle might purpose force because of issues. ‘

IPO marketplace situation

Regardless of the vulnerable benchmark and wide marketplace tendencies, the principle marketplace will upward thrust. Subsequent week, 8 new public problems will open. Of those, simplest the ₹ 126 crore IPO of Amaanta Healthcare from the mainboard will open on 1 September. The remainder seven problems will probably be from the SME section. Those come with Rachit Prints, Goel Development, Optivalue Tek Consulting, Austere Techniques, Vigor Plast India, Sharma Metals and Vashishtha Luxurious Model.

With the exception of this, the IPO of Oval Initiatives Engineering, Sugs Lloyd, Snehaa Organics and Abril Paper Tech will probably be closed subsequent week. On the identical time, Anlon Healthcare and Vikran Engineering will probably be indexed at the mainboard on 3 September, in addition to 11 listings will probably be observed within the SME section.

Technical perspective

Technical charts are indicating that Nifty 50 is these days vulnerable. On Friday, the index took trendline enhance at the remaining foundation but it surely remained under the quick -term transferring moderate. The trend like ‘Taking pictures Megastar’, made ultimate week, is indicating Barech Reversal. The unfavourable crossover in MACD and RSI’s lasting at 49.7 is appearing weak spot. If the index is going under 24,400, then a low take a look at of August is also. On the identical time, it’s imaginable to transport as much as 25,000 on crossing 24,700 upwards.

F & O Developments and Voltyness Index

Choices information presentations that there’s robust resistance for Nifty at 24,500-24,600. A rally is imaginable simplest after status on most sensible of it. The enhance is visual at 24,400-24,300 after which immediately at 24,000. India Vix rose 0.21 p.c to 11.75 this week. Because of low volatility, there’s a possibility of speedy transfer out there in any route.

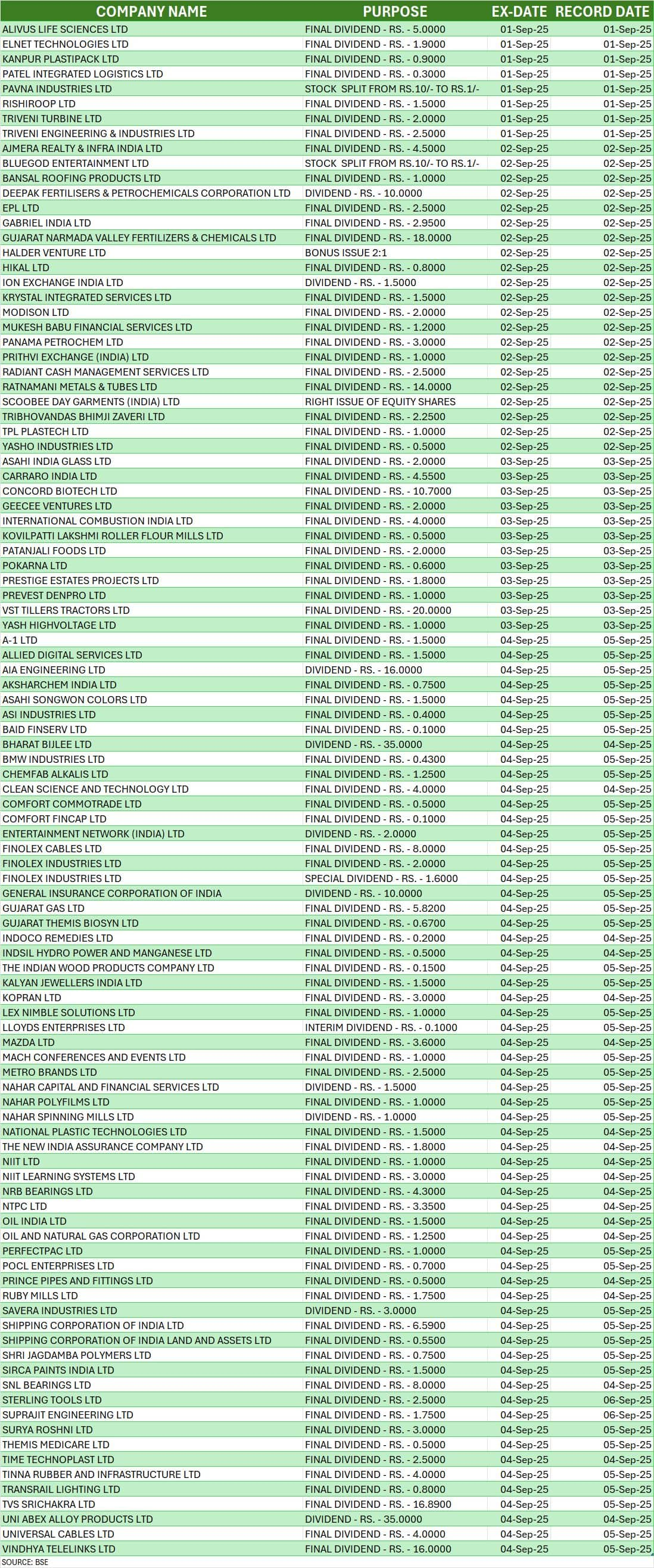

Company motion

Subsequent week, many firms also are fastened at company motion like dividend and bonus stocks, which will probably be monitored by means of traders. (See chart)

Disclaimer: Recommendation or concept mavens/brokerage corporations given on Moneycontrol.com have their very own private perspectives. The website online or control isn’t chargeable for this. Moneycontrol advises to customers that all the time search the recommendation of qualified mavens prior to taking any funding choice.